Note: This page includes content from the Integrated Report 2026.

Increasing the Quality of

Management Starting with

Capital Efficiency and

Accelerating Enhancement

of Cash-Generating

Abilities and Growth Investments

Under our Long-Term Corporate Strategy “R.I.S.E. 2035”, we have assessed the profitability of each business using ROIC as an important indicator and have subsequently undertaken overhauls of our businesses from the viewpoint of capital efficiency. While we are going to be undertaking overhauls including scale-downs and withdrawals in domains where it is unlikely that we will see the kind of profitability we expect, we are also working on the improvement of our earnings structure by allocating management resources in a focused manner to fields where we have a competitive advantage.

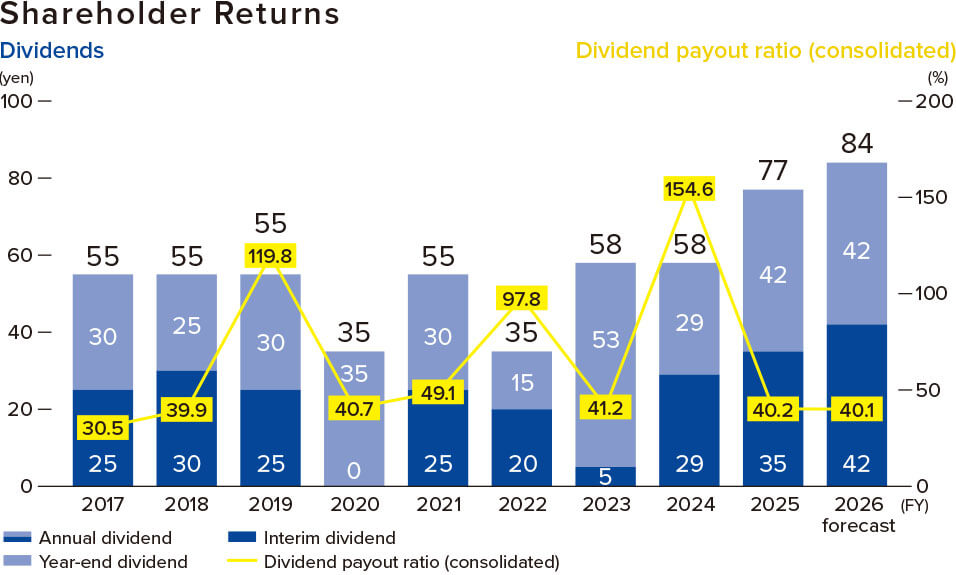

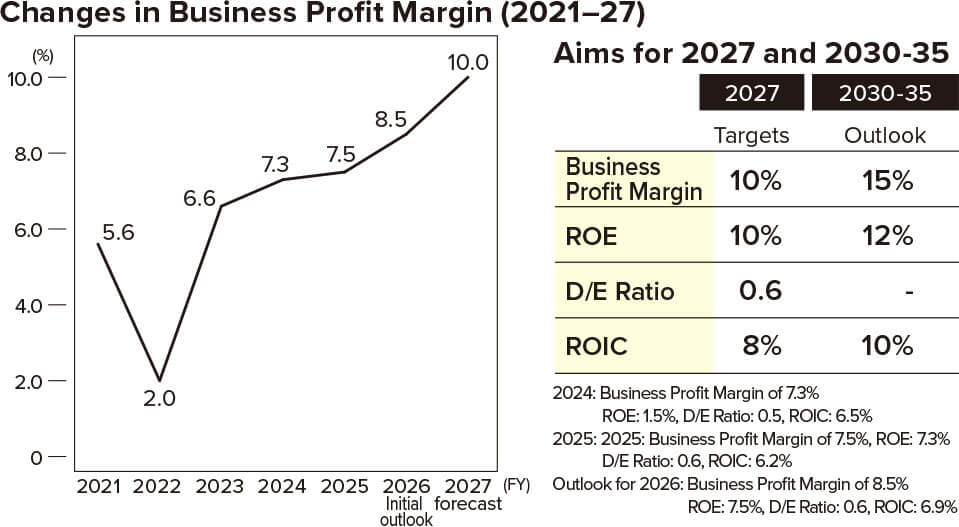

In addition to these business overhauls and the optimization of resource allocation, we have also been working on making progress with creating premium tire products and with cost reductions, resulting in a significant improvement in terms of business results for FY2025. We saw the success of our strategy of making premium tire products, which was led by our new product SYNCHRO WEATHER (which incorporates our proprietary ACTIVE TREAD technology), and saw sales revenue surpass our forecast reaching ¥1,207.1 billion in 2025. We also recorded our highest-ever business profit in the amount of ¥90.8 billion. Our business profit margin was 7.5% and improved for the third year in a row. In association with this, our net income was ¥50.4 billion, which was more than the figure in our forecast; given this, we have increased the annual dividend by ¥7 from the previous forecast to ¥77 per share.

While there were concerns about the impact of US tariffs during 2025, we were able to rebound from the impact of those tariffs as a result of having worked company-wide on price pass-through and the reduction of costs in relation to the financial impact equivalent to ¥13 billion. In addition to that, we started a total cost reduction initiative called Project ARK in July, which alone has resulted in a profit improvement surpassing ¥2.8 billion.

Meanwhile, with respect to capital efficiency, our ROE and ROIC for FY2025 were 7.3% and 6.2%, respectively. In addition to having completed our targeting of around 10 businesses and product lines for structural reform, we have been working on the improvement of capital efficiency by continuing with monitoring using ROIC as an indicator. Going forward, we will place importance on ROIC in relation to the decisions on investments in each business and firmly reflect the improvements in capital efficiency upon decision-making undertaken for management.

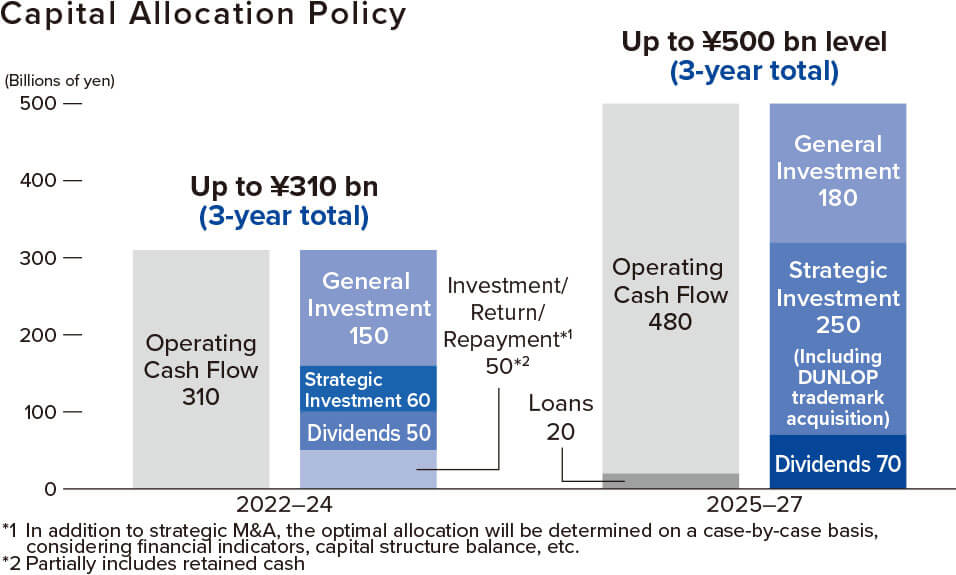

A significant turning point in terms of the further improvement of our earnings structures was the acquisition of the DUNLOP trademark rights and other assets in the regions of Europe, North America, and the Oceania region. While the acquisition amount for the brand and other elements temporarily meant a significant investment undertaken in the amount of approximately ¥100 billion, we see this as an extremely important strategic move for the improvement of our corporate value over the long term. Having become able to undertake the unified implementation of a brand strategy on a global basis means that we are able to optimize our product deployment and marketing investments with an even higher degree of freedom, meaning that we can expect the enhancement of our earning power to take place through the improvement of brand value.

Given that we are in the midst of establishing a foundation which serves to continuously generate stable cash flows through the acquisition of the DUNLOP trademark rights and other assets, our stance will have us stably improving upon corporate value by firmly tying cash flows produced by virtuous cycles to investments that will lead to medium-to-long-term growth.

Unit price improvements undertaken by creating more premium products in the Tire Business constitute a key driver of the enhancement of the Company’s profitability. We are moving forward with a shift to an earnings structure which is not dependent on the number of items sold, which is something we are doing by deploying products with high levels of added value and which leverage our ACTIVE TREAD technology on the foundation of the value of the DUNLOP brand. The composition ratio of premium products in the tire segment increased to 47% in 2025 and in 2026, our outlook is that we will break through 50%.

The new product group represented by SYNCHRO WEATHER is to serve as the core of our efforts to produce more premium products. The SYNCHRO WEATHER product launched in Japan in 2024 has expanded to 112 sizes in 2026 from the 100 sizes that were available as of the end of 2025. We plan to gradually deploy the product for the European and North American markets going forward. Through this effort, we will expand sales opportunities in high value-added markets and have that lead to an even further improvement of profitability.

Furthermore, we have been moving forward with the enhancement of business foundations in the premium domain through efforts such as the expansion of supply for premium new car manufacturers in Europe and through investment in tires with large diameters. Through these efforts, we are aiming to increase the composition ratio even more for high value-added products and shift to a portfolio which stably generates earnings. Going forward, we will also promote a unified premium strategy for the areas of brands, technologies, products and markets, and have that lead to further enhancement of our profitability.

Through the promotion of these strategies, we will steadily aim to accumulate business profits starting in 2026. Our stance is that we will go about improving profit rates in relation to the business profit margin of 7.5% from 2025 and setting our sights on increasing it to over 10% by 2027 and to 15% by 2030. Together with this, we are seeing the accumulation of more than 80% in terms of the implementation of ¥30 billion in target cost reduction effects for 2027 when it comes to Project ARK as well and will aim for even further profit increases by continuing to implement measures and ideas.

Deciding on which domains to allocate generated cash flows to achieve future growth is something which I think constitutes the most important management decision impacting corporate value. In terms of finance, we ensure that management is undertaken on the foundation of cash flows and thereby go about contributing to the improvement of corporate value by conducting investment decisions with an awareness of capital efficiency.

When making investment decisions, we place ROIC as a key indicator and thoroughly conduct screening based on the profitability and capital efficiency of each business. While on the one hand we will invest capital proactively in domains where it is likely that we will seethe kind of returns we expect, on the other, we will conduct balanced capital allocation through efforts such as overhauls of domains where improvements in profitability are not likely to be seen. Our aim is to build a business portfolio that is able to sustainably generate cash flows through disciplined investment decisions like these.

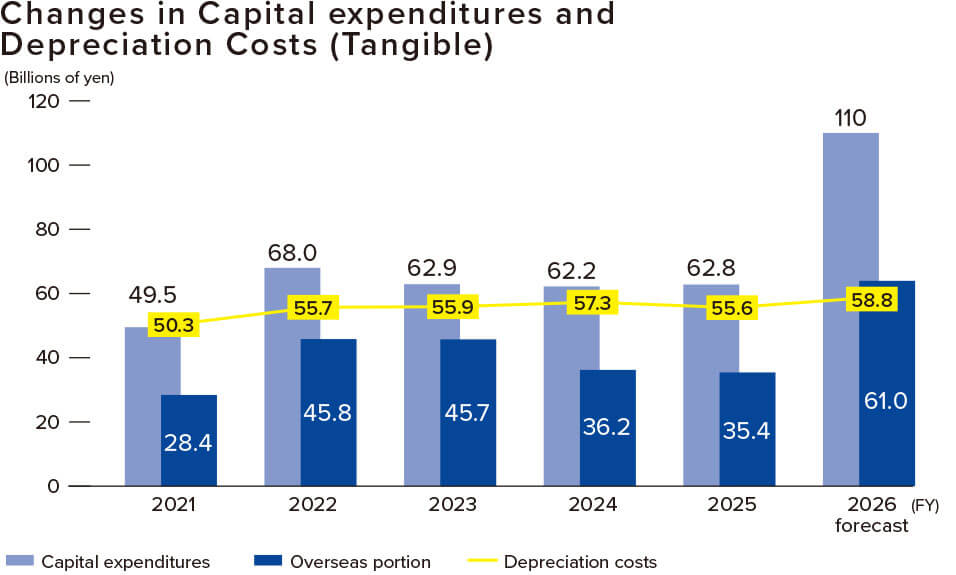

For growth investments, we will first put the highest priority on the enhancement of the premium domain in the Tire Business and move forward with the optimization of production allocation serving to support that, and with strategic investments into domestic factories. After having done so, we will proactively implement investments into fields to serve as future sources of earnings in non-tire businesses as well and aim to make our earnings base multi-layered. To be specific, we will move forward with the building of an optimal production framework while we deploy the DUNLOP brand globally, and also implement in a planned manner, initiatives such as investments into upgrades for aging equipment at factories in Japan and abroad.

Moreover, when it comes to capital allocation, we place an importance on the balance between growth investments and shareholder returns. We will, with the continuation of stable dividends serving as a foundation, work on the enhancement of shareholder returns in accordance with the improvement of our revenue generation capabilities. In terms of dividends, we will also incorporate a mindset of having at least 3.0% DOE starting in 2026 with the rule being that the consolidated dividend payout ratio will be at least 40%. This is a policy aimed at conducting stable returns to shareholders even in situations where there have been, hypothetically, significant drops in net income. Moreover, we will make timely decisions with respect to the effectiveness of share buybacks based on the investment opportunities and financial conditions that are present.

Going forward, we will further deepen dialogue with investors in relation to mindsets pertaining to management undertaken on the axis of capital efficiency and cash flow generation abilities. Together with appropriately communicating information on the intentions of management, and on initiatives being undertaken, we will drive sustainable improvement in corporate value based on the assessments and expectations of the markets.